NOTE: This comment is an update to the January 2018 article “Income Inequality puts Everything We Value at Risk”

In an unusual, unexpected, and bewildering press release, U.S. Treasury Secretary Steve Mnuchin announced on Christmas Eve that he has made phone calls to the “CEOs of the nation’s six largest banks” and that they have “confirmed ample liquidity is available for lending to consumer and business markets.”

While the release appears to be designed to ease concerns, it has done the opposite, as the issue of major banks’ liquidity had not been widely reported as a concern. There are serious concerns about the state of financial markets, as 2018 has been a baffling year for investors as 8 major asset classes have all struggled to make or hold gains.

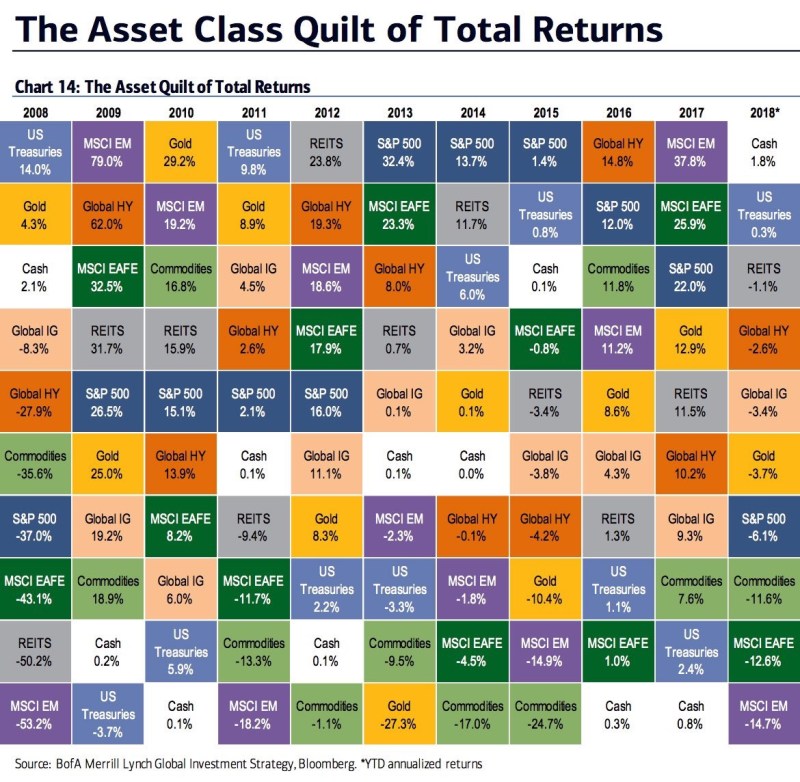

This “quilt” graphic shows 8 of 10 major asset classes down for 2018. CNBC went on to report (under the quilt graphic) that:

It’s not just that nothing’s working, investors are also for the first time in a long time losing a lot of money . The Russell 2000 and the Nasdaq Composite both dipped into bear market territory this week.

Blaming the Fed is inappropriate, given finance appears unable to function without historically anomalous post-2008 public assistance.

- A major structural driver of financial-sector stress is lack of wage growth, relative to cost of living.

- If investors want to see steadily expanding returns & rescue from the current leverage trap, they need to privilege investments that raise incomes.

- Because most people don’t gain more from capital investment than from work, expanding income inequality & the falling labor share of income are putting the long-term Main Street middle-class economy at risk.

- This makes consumers harder to find & new capital income less likely. (Scroll up for more on this subject.)

Axios is reporting today that 2019 could be the worst year for the US economy broadly since 2008, when the subprime mortgage bubble burst and the financial system went into near collapse.

- A critical detail of that report is that “If the Dow and S&P 500 finish at their current levels, they’ll have their worst December since 1931, during the Great Depression.”

- The economy works well when money keeps moving and wealth flows to value-creation in everyday lived experience.

- Right now, there is serious doubt as to whether the financial sector is positioned to support such a dynamic in the coming months.

- A key question is: How deep and far-reaching will the correction be?

As we noted 11 months ago (above):

The correction could be a blip of one or two days, or a prolonged malaise with uncertain causes. But pressures rippling out from the mounting imbalance will likely moderate long-running gains.

If the US is facing a liquidity crisis (or credit crunch), it will be strictly because too many of the structural, fiscal, and direct incentives driving financial decision-making skew toward industries that are over-dependent on easy capital and externalization of cost and risk. By contrast, Main Street businesses are a lower priority for lenders and are routinely forced to carry most of their own cost and risk.

We need new market signals that redirect investment toward more efficient ways of providing value to the general marketplace, so smaller value, more distributed and local actors that carry their cost and risk are empowered to drive expansion of incomes and local economies.