Climate stress, compounding costs & the greening of capital, are all picking up speed. Every actor, in every sector, needs to join the Race to Zero.

As global average temperatures continue to rise, due to still expanding carbon pollution, the risk, cost, and impacts of climate disruption are getting worse. More regions are now seeing regular, various, and overlapping climate disruption impacts—including summer and winter storms, drought and flooding, degradation of ecosystems, and firestorms big enough to make their own weather.

Some of these impacts are clearly already compounding each other’s effects. That we can see compounding climate impacts so visibly, in direct human experience, now, at roughly 1.2ºC of global heating, means we will be seeing far higher climate emergency costs even in the best case scenario.

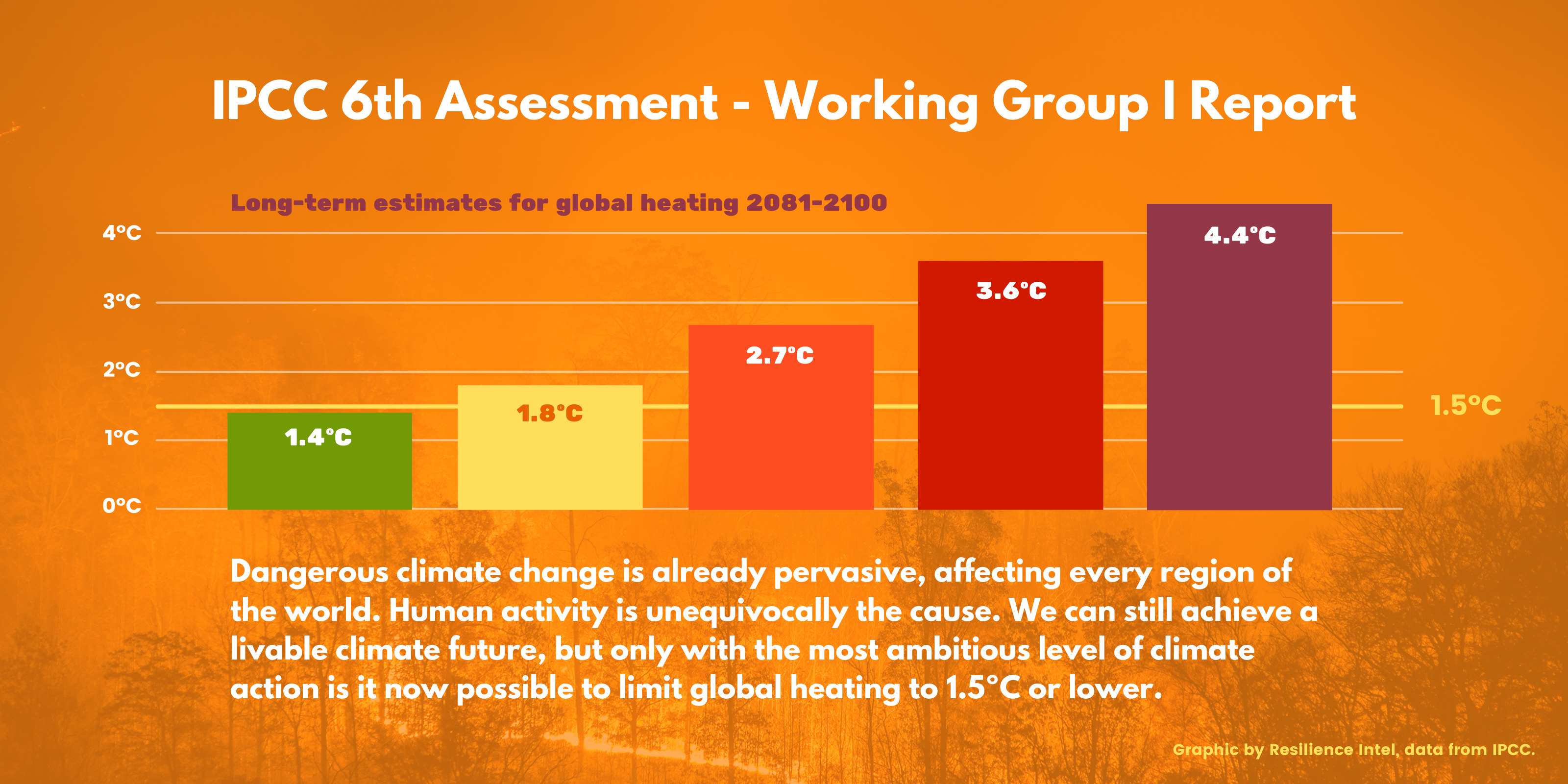

In its landmark August 2021 report on the physical science basis for the 6th Assessment, the Intergovernmental Panel on Climate Change examined all historical observations and projected 5 possible futures, based on the best scientific evidence. Of the 5 futures examined, only the one in which the world’s nations and industries successfully execute high ambition climate policy and innovation everywhere, sustainably, starting right now, can we limit global heating to 1.5ºC or less in the year 2100.

Even in that best-case scenario, we will breach 1.5ºC before nature draws down enough heat-trapping gases to bring us below 1.5ºC. We are seeing compounding effects now. Destabilization of the climate system will continue to add to this compounding effect. 1.6ºC won’t be 33% worse than 1.2ºC, but potentially several times worse in terms of harm and cost.

We should expect entire “breadbasket” regions will fail—possibly beyond just annual crop failure, but suffering ongoing, deep degradation—putting the global food supply at risk. We should expect mass migration on a scale not previously seen, and the failure of nation states, including some not considered now to be at risk of political or economic collapse.

Just as financial institutions have learned to track cascade effects of financial activities on financial returns under various asset classes, they will now need to learn to track geophysical cascade effects moving through natural systems, supply chains, and the operations and priorities of their peers and rivals. Those climate-related cascade effects are reshaping underlying value already, and will be factored into overall accounting of holdings and prospects, across sectors.

This unnecessary leakage of capital will reduce that market’s ability to invest in innovation and secure a future of climate-smart prosperity. That leakage of capital and innovation lag, together with expanding costs from health-related, economic, and political impacts of worsening climate disruption, will increase the cost of borrowing and further undermine that market’s competitiveness.

This will seem like a very different future to many in the financial sector, because the world’s ongoing dependence on fossil fuels and the dynamics of commodity markets still provide opportunities for financial windfalls. The problem is: Those opportunities are becoming fewer and more uncertain, and this other future must and will take over; there is no viable future economic scenario in which the status quo holds.

In 1992, the nations of the world agreed to “prevent dangerous anthropogenic interference with the climate system”. In 2015, the Paris Agreement updated that framework so every nation had a role to play and a way to prosper by helping to prevent danger for everyone.

In Glasgow, next month, nearly 200 nations will gather with thousands of expert observers to significantly upgrade global ambition, with an aim to achieving that best of 5 futures examined by the IPCC. Already, $88 trillion in wealth is committing to align with that future, through the Glasgow Financial Alliance for Net Zero (GFANZ).